Telco 2.0™ Research

The Future Of Telecoms And How To Get There

The Future Of Telecoms And How To Get There

|

Summary: In this new report based on Telco 2.0 Transformation Index analysis we compare Vodafone’s competitive positioning with another European-centric multi-national, Telefonica. The results are surprising and instructive, showing that Vodafone faces substantial challenges if it is to grow in the foreseeable future. (April 2014, Executive Briefing Service, Transformation Stream.) |

|

![]()

![]()

Below is an extract from this 20 page Telco 2.0 Report that can be downloaded in full in PDF format by members of the Telco 2.0 Executive Briefing service and the Telco 2.0 Transformation stream here. We'll also be exploring the implications at the OnFuture EMEA 2014 Brainstorm in London, 11-12 June. For more on any of these services, please email / call +44 (0) 207 247 5003.

To share this article easily, please click:

Introduction

As part of the recently launched Telco 2.0 Transformation Index, STL Partners has been analysing the transformation efforts of major telecoms operators. We are close to completing a major analysis report on Vodafone which will complement those already completed for Telefonica, SingTel, Verizon, AT&T and Ooredoo. Vodafone’s scores will also be added to an update of the Benchmarking Report which will be released in May.

The full analysis of each player covers 5 domains:

In this report we explore a small part of the Marketplace analysis for Vodafone and compare its competitive positioning with another European-centric multi-national, Telefonica.

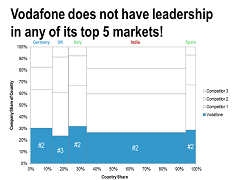

The results, we think, are surprising and instructive. Vodafone, often held up as the strongest and most global player, actually has relatively weak competitive positions in its leading markets (it does not hold market leader positions) and is exposed to structurally competitive markets (even those that are developing). Within this context, the company faces substantial challenges if it is to grow in the foreseeable future.

Of course, this is a small extract of a much deeper analysis on Vodafone. In the full report, we explore Vodafone’s growth and transformation strategy in full and make specific recommendations on 3 different strategic options for management.

STL Partners full report on Vodafone and Telefonica covers four areas of analysis within the Marketplace domain:

The overall health of the economies in which Vodafone and Telefonica operate as reflected by GDP size and growth.

The digital maturity of Vodafone's and Telefonica’s markets as reflected by consumer and enterprise adoption and usage of telecommunications and internet services.

The regulatory framework that Vodafone and Telefonica operate within. Includes legislation and attitudes to pricing, net neutrality, CSP technical and commercial collaboration for new Telco 2.0 solutions, etc.

The nature of competition - how players compete, their goals, the strategies they deploy, the products they develop

How Vodafone and Telefonica are competing in the marketplace and their strengths and weaknesses

What customers want and, more importantly, are trying to achieve (physically, intellectually, socially) and how this is reflected in their (digital) behaviour including how they use products, react to companies and brands, share information about themselves etc.

Specifically, the regard with which customers hold Vodafone and Telefonica

For the purposes of this report, we have extracted elements of the full analysis and present them along two dimensions: Market Attractiveness (the underlying growth, maturity and structure of Vodafone and Telefonica’s markets) and Competitive Position (Vodafone and Telefonica’s relative strength within these markets).

We explore a number of individual metrics within each dimension and, as we show in Figure 1 below, have collected data for each operator and then evaluated which of the two is in a stronger position. Setting aside the three metrics where the CSPs are broadly at parity, at a summary level it appears that Telefonica appears to be in a stronger position than Vodafone:

Telefonica’s markets look more attractive than Vodafone’s: Telefonica outscores Vodafone by 6 metrics to 2 for Market Attractiveness including for GDP growth, GDP per capita growth, Bank account penetration, Broadband penetration, Herfindahl Score (a measure of a market’s structural attractiveness) and Mobile revenue growth. Vodafone’s markets, by contrast, are only more attractive than Telefonica’s in terms of overall GDP size and Internet penetration.

Telefonica’s competitive position appears to be stronger than Vodafone’s: Telefonica outperforms Vodafone in 4 out of 6 metrics including ARPU as % of GDP per capita (ie share of wallet), market share, market position in top 5 markets, market share gain/loss. Vodafone only outperforms Telefonica in 2 metrics: Total subscribers and Facebook penetration (with a lower penetration acting as a proxy for weaker OTT competition).

The ‘tale of the tape’ in Figure 1 is a top-line snapshot. The rest of this report digs into a few of the metrics in more detail and seeks to explain where and how Telefonica is enjoying an advantage over Vodafone.

Source: Company accounts; Market regulators, World Bank, International Monetary Fund, ITU, Internetworldstats.com, Benchmarking telecoms regulation – The Telecommunications Regulatory Governance Index (TRGI) by Leonard Wavermana, Pantelis Koutroumpis (published by Elsevier 2011) STL Partners analysis

To access the rest of this 20 page Telco 2.0 Report in full including...

Telefonica is more exposed to fast-growing emerging markets

Vodafone has only 30% of revenue in emerging markets…

…compared with over 50% for Telefonica

Telefonica’s Latin American markets have grown much quicker than Vodafone’s Emerging ones…

…and Telefonica’s European markets have contracted at a similar rate to Vodafone’s Developed ones

Telefonica’s has a stronger competitive position than Vodafone in the most important markets

Overall, Telefonica has a stronger market position and is performing better in more attractive markets than Vodafone

...and the following report figures...

Figure 1: Telefonica and Vodafone Market Attractiveness and Competitive Positioning – The Tale of the Tape

Figure 2: Vodafone subscribers and revenue

Figure 3: Telefonica subscribers and revenue

Figure 4: Vodafone and Telefonica mobile market growth

Figure 5: Market shares in top 5 revenue-generating markets

Figure 6: Market Positioning Maps

Figure 7: Overall, Telefonica enjoys a 56% advantage over Vodafone using STL Partners’ Market Attractiveness-Competitive Situation (MACS) score

Figure 8: Portfolio Strategy Maps

Figure 9: Telefonica’s performance is broadly neutral and Vodafone’s negative using STL Partners’ EBITDA Margin-Market Share (EMMS) score

...Members of the Telco 2.0 Executive Briefing Subscription Service and the Telco 2.0 Transformation stream can download the full 20 page report in PDF format here. Non-Members, please subscribe here. For other enquiries, please email / call +44 (0) 207 247 5003.

Technologies and industry terms referenced include: Vodafone, Telefonica, Telefonica, SingTel, Verizon, AT&T, Ooredoo, Telecoms, Strategy, Transformation, Operator, Telco, Business Model