Summary: It can be tempting to think of Android as in a two-horse race with Apple. Our analysis shows that the current and future impact of Google's highly successful mobile ecosystem play is much more complex.

|

This is an extract from this Telco 2.0 Executive Briefing that can be accessed and downloaded in full in PDF format by members of the Telco 2.0 Executive Briefing service and the Telco 2.0 Disruption Stream using the links below. 'Lessons from Apple: Fostering vibrant content ecosystems' is also a key session theme at our upcoming 'New Digital Economics' Brainstorms (Palo Alto, 4-7 April and London, 11-13 May). Please use the links or email [email protected] or call +44 (0) 207 247 5003 to find out more. |

Android, the Google-backed, Linux-based mobile operating system, has been an enormous hit. We predicted this, but we didn't predict the explosive growth that the platform has experienced in the past 12 months. Whichever metric you choose – shipments, ad-serving, traffic – has been growing exponentially. Google chairman Eric Schmidt said at Mobile World Congress 2011 that Android device activations were running at 300,000 daily, making it by far the fastest growing mobile platform, and that some 170 devices are now available from 27 vendors.

At the same time Android has been expanding horizontally, becoming a platform for tablets, media devices, connected-TV set top boxes, and even military applications.

Google clearly wants to extend its dominance of search-related advertising into the mobile market and Android is becoming a potent weapon with which to fend off potential challengers, such as Apple, Nokia and Facebook. Apple has demonstrated the value of integrated content/software/delivery systems and Google has rightly perceived the combination of iTunes, iAds, and the iOS devices as a major competitive threat. Moreover, Apple’s focus on apps, rather than web browsing, threatens to weaken the strategic position of Google’s search engine.

Rather than pursuing a “fast follower” strategy of trying to replicate the Apple system, though, Google opted for an “asymmetric insurgent” strategy of trying to disrupt it by spreading Android. Although, with the Nexus One, Google experimented with creating their own channels to market for Android devices, for the most part it has let Android off the leash, allowing all-comers to use it and customise it as they see fit.

One upshot – which we weren't expecting – is that it's ceased to be described as “Google Android”. At the outset, Android could have proven to be just another interesting Google project (one of those ‘submarines’ we described in our previous analysis), or else a strategic invasion of the carrier business model, with Google aiming to deliver an iPhone-clone that would be sold through their own channels.

Yet, despite the runaway success of Android, it’s arguable whether Google has even made a return on its investment in it yet.

Hence the question: why did Google do it? Our view is that Google has already reaped enormous strategic rewards - by making Android free, open-source and customizable, it has spread like a virus, contained Apple at the top end of the smartphone market, forced Nokia on to the back foot, and secured a foothold for Google in the mobile ecosystem. We also argue that it is still early days in their business plan, and that we expect Google to find more direct ways to monetise the platform they are building.

In the rest of this Executive Briefing, we examine the reason for Android’s success, its impact on the industry including Google, Google’s strategy with Android, and what telcos and others can learn from one of the first great ‘ecosystem plays’ of the mobile internet era.

We’ll be discussing more on ‘Fostering vibrant ecosystems’ at the New Digital Economics Executive Brainstorms (Palo Alto, 5-7 April, London 11-13 May 2011).

This is obvious and less compelling now that several other royalty-free mobile solutions are available. But it wasn't so obvious at the time of launch.

Everyone from Sony Ericsson to China Mobile to the US Special Operations Forces has customised Android. The US Special Operations Forces have apparently lost patience with the US Army’s procurement bureaucracy’s efforts to buy a new radio, and issued an RFP for a collaboration suite based on Android to work with their mesh-network radio system. Google probably wasn’t expecting that.

Android is, fundamentally, a Linux distribution and you can do almost anything you want with it. It also benefits from an enormous pool of Unix/Linux talent at every level from hardware to applications development. Hence the US Special Operations Command's decision to issue an RFP for a complex communications/collaboration toolkit and to specify that it should run Android. Also, it's quite possible to replace parts of its modular architecture. Myriad Group, for example, produces an alternative to the Google-controlled Dalvik Java virtual machine at the core of the Android programming environment.

While lagging behind Apple’s iOS, Android has benefited from a more intuitive user-interface than rival multi-vendor smartphone operating systems, such as Symbian and Windows Phone 6 (Windows Phone 7 is much more competitive). Unlike Symbian and Windows, Android was built from scratch to support touch-screens and has to date offered the most Apple-like experience of any of the mainstream smartphone operating systems.

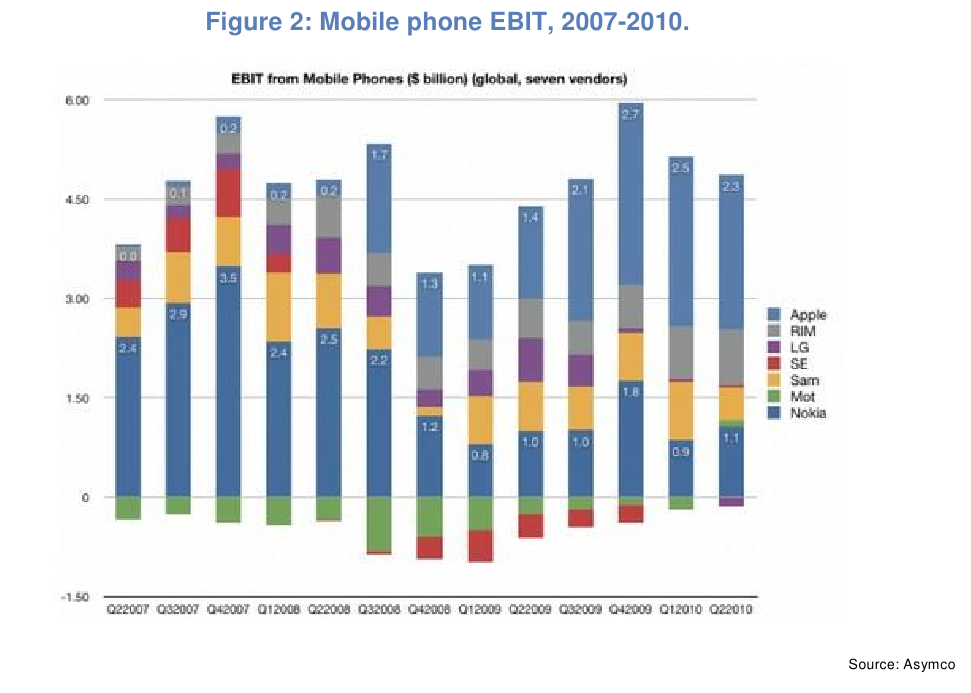

As a free, customizable and user-friendly operating system, Android has empowered many of the weaker hardware vendors. To recap, in the depths of the economic crisis, Nokia (in terms of market share) and Apple (in terms of profitability) ruled the world, the ultra-low cost market went to ZTE, and the midmarket was savagely squeezed, as the chart below clearly showed. In 2007-2009, Motorola and Sony Ericsson crashed into loss. At the same time, there was a mammoth reorganisation of the profit pool. Essentially, a large chunk of the profits that previously went to Nokia went to Apple, while RIM maintained a niche and Samsung garnered what was left in the middle.

Since then, the key midmarket vendors – Motorola and Sony Ericsson – have experienced an impressive comeback, through specialising in Android devices. As far back as September 2008, just as its business was falling off the cliff, Motorola was reported to have hired 350 Android engineers.

By 3Q10, Motorola had reported getting the handset division's losses down to the point where the network division's profits outweighed them again, and had stated that going forward, their other device classes will be discontinued in favour of concentrating on the Android platform. Sony Ericsson has since discontinued its UIQ fork of Symbian and scored a significant device hit with the Xperia X10 Mini. In early February 2010, Motorola Mobility reported profits for the first time in three years. HTC and Samsung have also embraced Android and, according to research firm Canalys, together shipped 45% of the total Android deliveries in the fourth quarter of 2010.

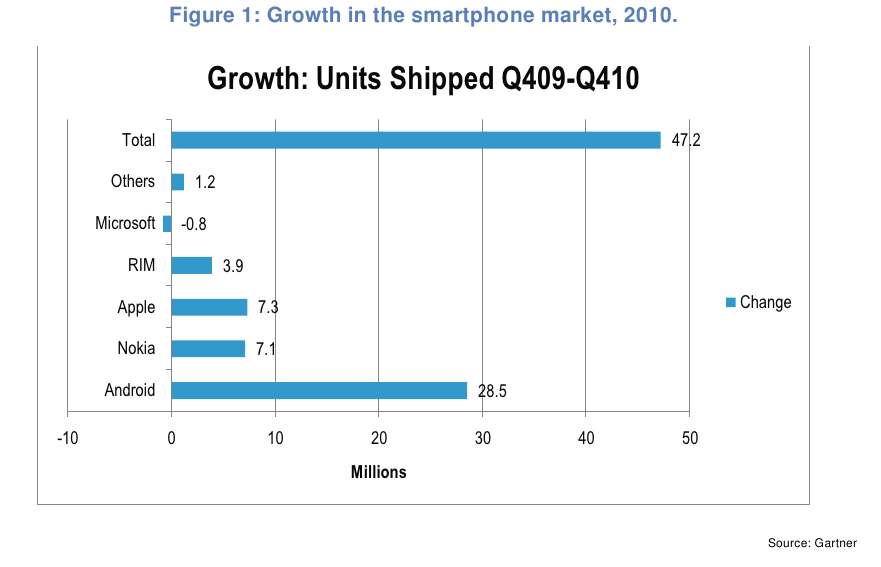

All this has happened against a backdrop of continued rapid growth in the smartphone market. The numbers of smartphone units shipped to end users rose 87% from the fourth quarter of 2009 to the corresponding period in 2010. Indeed, the only mobile OS platform that actually lost shipments was Microsoft Windows.

The picture in terms of market share, however, is very different. In the light of rapid growth of the entire sector, it was necessary for any given vendor to almost double their sales in order to keep up.

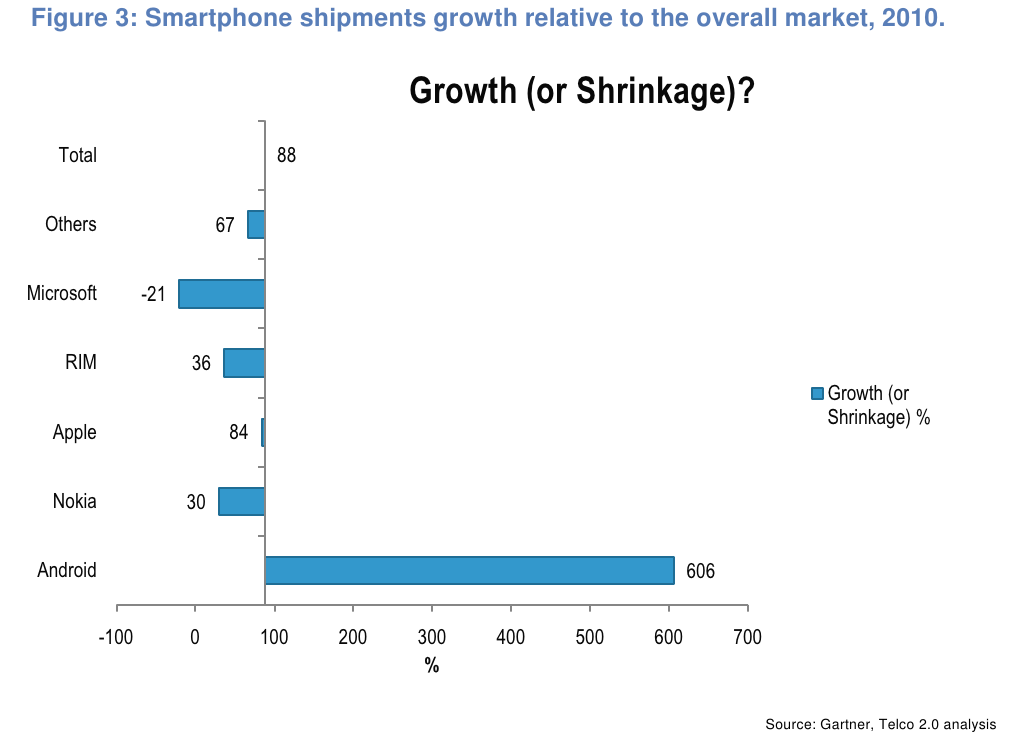

As the following chart shows, growth of the smartphone segment overall masks just how drastic the reorganisation has been. In this chart, we’ve rebased the vertical axis to place zero equal to the 87% year-on-year growth in smartphone shipments.

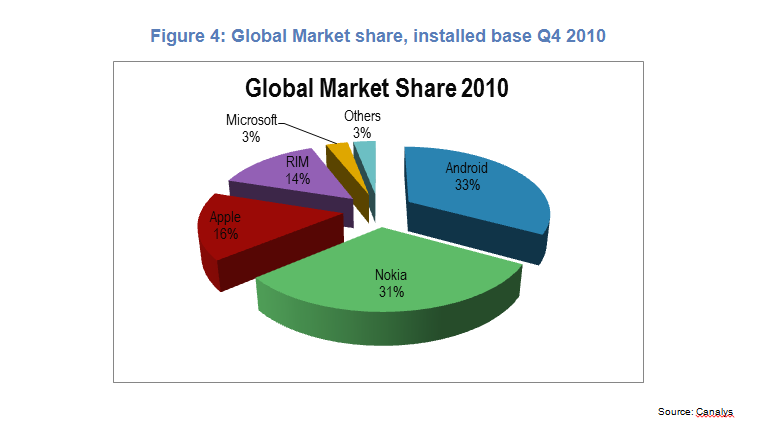

RIM, Microsoft and Nokia have given up substantial share, Apple has mostly clung on to the chunk of the market it seized in 2007, and Android has moved into first place. Android is now the leading smartphone platform (see Figure 4).

RIM, Microsoft and Nokia have given up substantial share, Apple has mostly clung on to the chunk of the market it seized in 2007, and Android has moved into first place. Android is now the leading smartphone platform (see Figure 4).

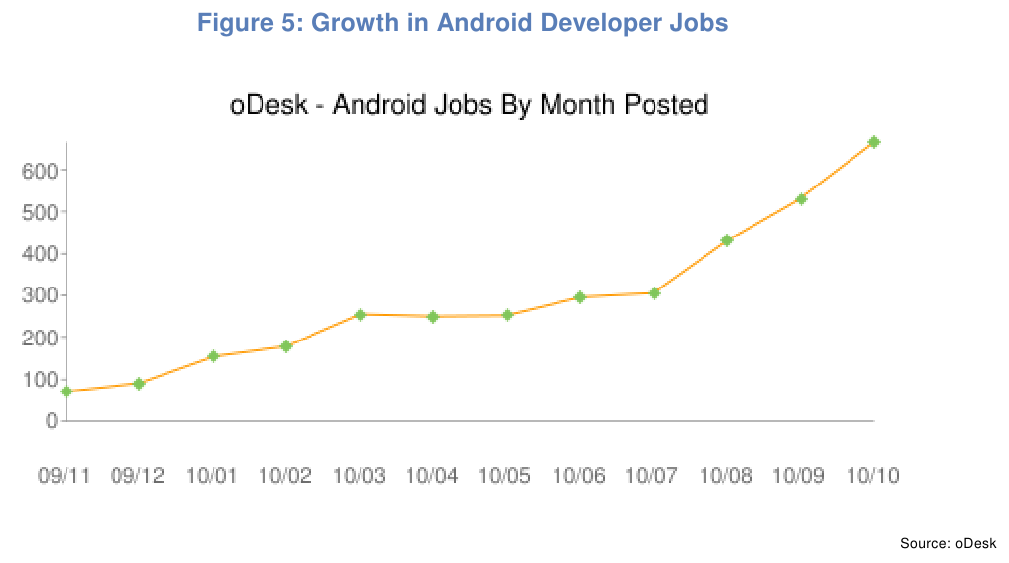

The arrival of Android has also boosted the software developer community. The following chart shows job advertisements for Android developers on a major industry website.

No device operating system has been more carefully designed to meet developers’ needs – its status as a Linux distribution, primarily using Java as the application development language (but not having any objection to development in native C++, Adobe Flash, HTML/JavaScript, or even Python through the Android Scripting Environment plugin) permitted a maximum degree of cross-over from the wider Unix/Linux world.

Developer user-experience studies carried out for Telefonica’s Bluevia programme suggest that the average time to learn Android is five months, compared to 15 for Symbian – we’re not aware what standard of proficiency this assumes, but it is certainly plausible. Symbian was, notoriously, the operating system that involved special seminars on how to use the string data type, something which is utterly trivial in every other programming environment.

Android’s development process and software development kits (SDKs) are excellent (you may recall our report Nokia vs. Apple: Lessons from the Smartphone Wars). As an example of simplicity in programming terms, the process of deploying test-stage software to a device is to issue the following single command-line statement:

Out of the big four mobile platforms, Android’s rise has checked Apple iOS’s growth and has set back RIM somewhat...so what impact has it had on Nokia? We now know the answer. With the Microsoft-Nokia deal, two of the players who fell behind the most (see figure 3) have formed an alliance, which from a software point of view means Symbian’s exit from the market. The first Windows-Nokia devices are not expected before December 2011, when a major (and repeatedly delayed) software update is planned. As a result, the “new” player is not going to be in the field for most of this year and the impact is already visible in the quarterly numbers. With Nielsen reporting that U.S. smartphone market share for everything other than Apple, Android, and RIM at 17%, and a significant fraction of that being made up of the run-off of Symbian devices, for Nokia it will be less a question of transitioning from Symbian ^3 to Windows Phone 7 as of re-entering the U.S. smartphone market from first principles.

So essentially, as well as putting the brakes on iOS at the top end of the market, Android has been the means for a competitive knockout of the biggest smartphone platform. It has since emerged that Nokia considered the possibility of becoming an Android OEM, but is rumoured to have been offered a substantial side payment from Microsoft as well as having reservations about becoming a purely ‘me too’ Android smartphone maker.

An interesting question here is to what extent Google has ever considered itself to be in competition with Nokia, and to what extent it would benefit from Symbian’s exit. The Nokia division that is most obviously competitive with Google – the navigation/mapping specialist Navteq – is protected by the Microsoft-Nokia deal, so Google hasn’t succeeded yet in neutralising that threat.

To read the rest of the article, including:

...Members of the Telco 2.0TM Executive Briefing Subscription Service and the Telco 2.0 Disruption Stream can access and download a PDF of the full report here. Non-Members, please see here for how to subscribe. Alternatively, please email [email protected] or call +44 (0) 207 247 5003 for further details. There's also more on 'Lessons from Apple: Fostering vibrant content ecosystems' at our AMERICAS and EMEA Executive Brainstorms and Best Practice Live! virtual events.